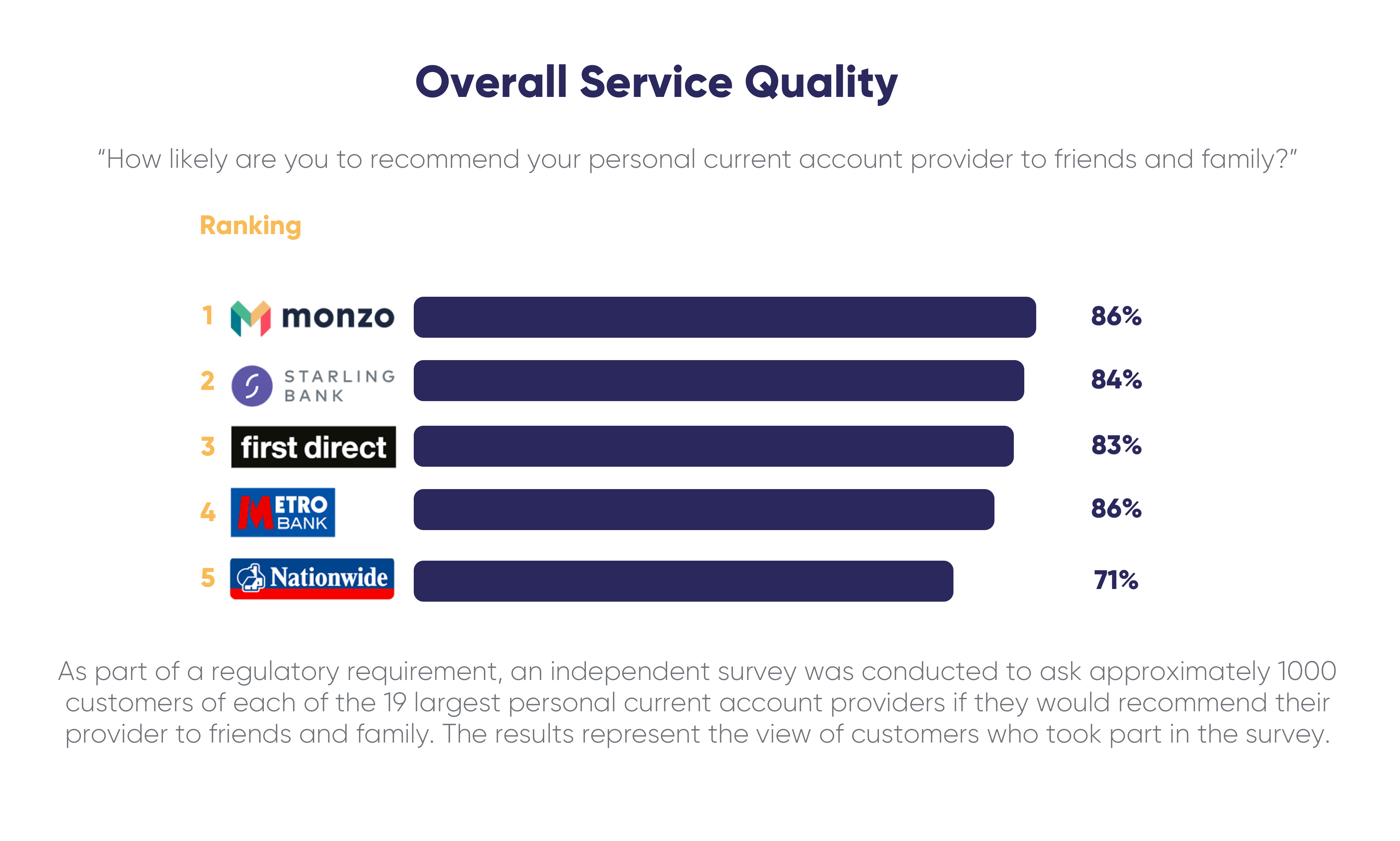

You may have seen that Monzo bank was rated first among the 19 largest personal current account providers by the regulatory ‘independent service quality survey’ in both its service quality and online services. This is a huge win for Fintech, as Monzo’s services beat out traditional brick and mortar banks, even some of the largest in the UK. These results highlight the competitive advantage modern Fintech providers have over more traditional financial services and underscore the importance of easy and intuitive mobile banking. In fact, a recent study revealed that 24% of banks’ revenue was lost to Fintech providers.

The intuitive use of Behavioural Science may be a competitive advantage in generating the best customer experience. Financial services such as Monzo, Starling, Moneybox and Plum have all expressed interest in Behavioural Science and have used behavioural principles to build their products. This helps in attracting and keeping customers. These techniques aren’t exclusive to Fintech, actually, many principles can be applied to all banking products to improve the overall customer experience.

Here Are Three Ways That Fintech Companies Are Implementing Behavioural Science:

1) Products that help us save money

Defaults & Present Bias

Pairing multiple biases together can make product features more intuitive and useful for customers. This works so well because products are made to complement natural human behaviour. People tend to go with the flow and don’t often go out of their way to change from pre-set courses of action. This is often referred to as the default effect. Furthermore, people have a natural tendency to prefer instant gratification instead of larger rewards in the distant future. This is known as the present bias. Saving money for the future can be thwarted by spending money in the present.

Fintech companies use defaults to combat users’ present bias in some of their products to help their customers save more money. For example, features like Monzo’s round-up savings. This automatically rounds up each purchase to the next pound, setting a default for the customer to save small amounts of their spare change. Daily saving then occurs with every purchase, which helps customers to build up their savings account consistently and avoid the temptation to put off saving their money. The brilliance of the feature is, users don’t have to actively think about saving. Instead, their account does it for them every time they spend.

2) Technology that is easy to use

Processing fluency

Processing fluency increases our ability to cognitively understand and enjoy any sort of stimulus. When a product is designed with this fluency, users gain more enjoyment while engaging with it, leading to an improved customer experience and a more loyal customer base. This has been found time and again by experimenters who have manipulated processing fluency using a vast array of techniques. For example, by merely changing fonts, letter spacing, and backgrounds users rate identical products differently based on how easy it is for them to quickly read and understand.

Often, financial information can be stodgy or confusing to consume. Fintech institutions use behavioural design to present their customer’s financial information with thoughtfully designed pages that have high overall high processing fluency. Customers can view their accounts or track their spending easily with intuitive icons and satisfying imagery. Fluent behavioural design helps users to visualize their money, making it easier for people to understand complex and important information such as their finances. All features are easy for users to access, no scrolling in a long list of menu options. This makes customers enjoy interacting with their mobile banking app more, giving them more satisfaction overall with their bank.

3) Features that are social

Social Influence

We are social animals, and enjoy interacting with our peers. When it comes to banking, Fintech has made it easier than ever to send money and split costs with friends and family. Fintech like Revolut makes it simple and secure to send money to others by saving the banking information of contacts. Users can scroll through their friends, and in two clicks send money. By keeping users’ account information, it makes it more convenient and social for banks. Some Fintech companies are taking these peer effects even further, like Flender that facilitate peer-to-peer connected borrowing and lending. While these services are newer, the growing popularity highlights the opportunity to make banking more social and easier for users to connect with others.

Peer effects are strong and can work as a marketing tool. We as humans are influenced by our peer group and often knowingly or unknowingly adopt the behaviours and beliefs of those we consider in our in-group. When a peer is using their banking app to quickly send funds after a group dinner, or for transferring their share of rent it can be a selling point for others to want to be able to enjoy the same benefits.

Conclusion

In conclusion, there are some impressive ways that FinTech has started to apply behavioural science to their products and services. There are even more avenues that can be explored by Fintech providers and traditional banks alike. Knowledge of behavioural biases, such as these 3 principles, can greatly improve customer outcomes from an improved daily experience to increased brand loyalty.

Using behavioural science in designing new products and upgrading existing features can help banks transform their offerings and grow their customer base. At Cowry, we can help banks utilise behavioural science in their digital customer experience from optimising a current feature to redesigning the end-to-end customer journey. Explore our case studies below, or get in touch if you’d like to learn more!

References:

Alter, A. L., & Oppenheimer, D. M. (2009). Uniting the tribes of fluency to form a metacognitive nation. Personality and social psychology review, 13(3), 219-235.

Huh, Y. E., Vosgerau, J., & Morewedge, C. K. (2014). Social defaults: Observed choices become choice defaults. Journal of Consumer Research, 41(3), 746-760.

Ipsos Mori. 2020. Personal Banking Service Quality. [online] Available at: <https://www.ipsos.com/ipsos-mori/en-uk/personal-banking-service-quality>

Johnson, E.J., & Goldstein, D.G. (2003). Do Defaults Save Lives? Science, 302 (5649), 1338-1339.

Loewenstein, G. & J. Elster, Eds. (1992). Choice over time. New York, Russell Sage Foundation.Strandvik, T., Holmlund, M., & Lähteenmäki, I. (2018). “One of these days, things are going to change!” How do you make sense of market disruption? Business Horizons, 61(3), 477-486.